Recording Business Transactions

Business Transactions

Recording ABC Transactions

Now, I think we should be ready to revisit our ABC Mowing Company and record the transactions presented in prior lessons in our detailed accounts.

We are going to assume that ABC has beginning balances already recorded in their accounts. These balances are as of December 1, xxxx.

Note: If these balances were as of the beginning of the year the nominal or temporary accounts – revenues, expenses, and draws would all have zero balances.

Lastly, we are going to thoroughly review each transaction for December xxxx and show you the hows and whys to properly recording each transaction and present the steps for properly analyzing and recording a transaction.

ABC’s Beginning Account Balances as of December 1, xxxx

| Assets | Liabilities | Equity | |||

| Cash | $5,500 Dr | Accounts Payable | $2,000 Cr | Owner's Capital | $7,500 Cr |

| Accounts Receivable | $1,600 Dr | Mowing Revenue | $1,000 Cr | ||

| Mowing Equipment | $2,500 Dr | Advertising Expense | $200 Dr | ||

| Inventory-Office Supplies | $-0- | Mulch Expense | $100 Dr | ||

| Owner Draws | $600 Dr | ||||

Notice I used the symbols Dr and Cr to abbreviate the Debit and Credit balances in the table of ABC’s beginning balances. While this is a common method of representing debits and credits, other symbols that we discussed earlier are also used.

You’d better check me out to see if our books balance before we start recording ABC’s transactions. We’re going to perform two checks that relate to what we’ve been learning in prior lessons.

The first check is to see if our Accounting Equation balances and the second to make sure that the debit balances equal the credit balances.

Equation Check Calculations

Total Assets = Cash + Accounts Receivable + Mowing Equipment

Total Assets = 5,500 + 1,600 + 2,500

Total Assets = 9,600

Total Liabilities is easy because there is only one account (Accounts Payable) with a balance of 2,000.

Total Liabilities = 2,000

Total Equity = Owner’s Capital + Revenues – Expenses – Draws

Since we have more than one expense let’s summarize them before we use them in our equation.

Total Expenses = Mulch Expense + Advertising

Total Expenses = 100 + 200

Total Expenses = 300

Total Equity = Owner’s Capital + Revenues – Expenses – Draws

Total Equity = 7,500 + 1000 – 300- 600

Total Equity = 7,600

Substituting our totals into the Accounting Equation we find that our equation balances.

Assets = Liabilities + Owner’s Equity

9,600 = 2,000 + 7,600

Our second check is to see if our debit account balances equal our credit account balances.

| Debit Balances | |||

| Cash | 5,500 | ||

| Accounts Receivable | 1,600 | ||

| Mowing Equipment | 2,500 | ||

| Advertising Expense | 200 | ||

| Mulch Expense | 100 | ||

| Owner's Draw | 600 | ||

| Total Debits | 10,500 | ||

| Credit Balances | |||

| Accounts Payable | 2,000 | ||

| Owner's Capital | 7,500 | ||

| Mowing Revenue | 1,000 | ||

| Total Credits | 10,500 | ||

It looks like we passed muster again. Debit Balances do equal Credit Balances.

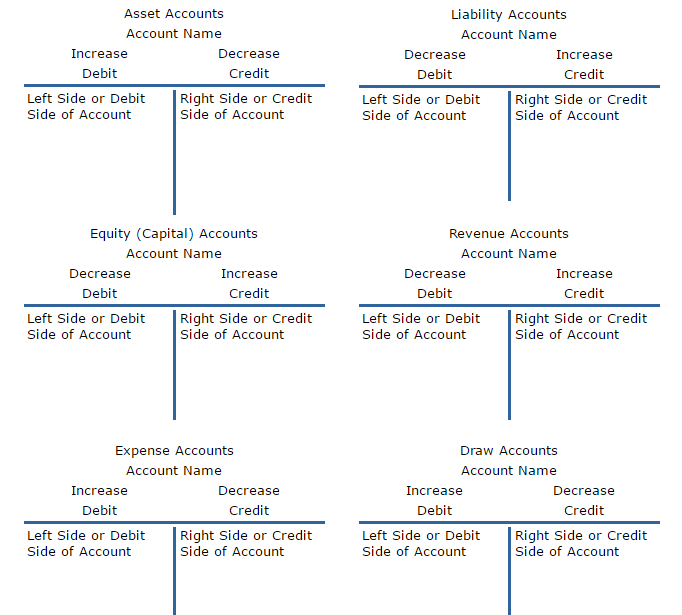

We will discuss each transaction and “post” the entry to the appropriate General Ledger Account

( T-Account). Keep in mind that each entry will have a debit and a credit.

If you recall, a T-Account is a skeleton outline of a formal account which provides the same basic data as a formal ledger account. They are normally used as a teaching aid. In a later lesson we'll be using formal ledger accounts. The following is what the T-Accounts look like.

Notice that Assets, Draws, and Expense Type of Accounts are increased using the Left Side (Column) of the account ( debited ) and decreased using the Right Side (Column) of the account ( credited ).

The reverse is true for the Liability, Equity, and Revenue Type of Accounts. These Type Of Accounts are increased using the Right Side (Column) of the account ( credited ) and decreased using the Left Side (Column) of the account ( debited ).

Detail Transaction Information

For each transaction for ABC Mowing, we will identify the Source Document, Type Of Transaction, Accounts Affected, and determine and explain the Debits and Credits needed to properly record and post to our General Ledger (T-Accounts).

Entry 1

1. ABC mows a client’s yard and receives a check from the customer for $50 for the service provided.

Source Document:Customer’s Check

Type Of Transaction:Cash Sale

Accounts Affected:Cash Sales

Debits and Credits:

Increase (Left Side) Cash: Debit

Increase (Right Side) Mowing Revenue (Sales): Credit

Explanation Using Our Debit/Credit Rules:

The Asset Account Cash is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of cash, which is an asset, is the left (debit) side of the account so we increase cash by entering the amount in the left side as a debit.

The Revenue Account Mowing Revenue (Equity) is also increased. Again, an increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of a revenue account is the right (credit) side of the account so we increase mowing revenue (sales) by entering the amount in the right side as a credit.

Entry 2

2. ABC purchases $100 worth of office supplies and stores them in their storage room. The office supply store gives them an invoice that allows them to pay for them in 15 days (on account).

Source Document:Supplier’s Invoice

Type Of Transaction:On Account Purchase

Accounts Affected:Inventory-Office Supplies Accounts Payable

Debits and Credits:

Increase (Left Side) Inventory-Office Supplies: Debit

Increase (Right Side) Accounts Payable: Credit

Explanation Using Our Debit/Credit Rules:

The Asset Account Inventory-Office Supplies is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of inventory-office supplies, which is an asset, is the left (debit) side of the account so we increase inventory-office supplies by entering the amount in the left side as a debit.

The Liability Account Accounts Payable is also increased. Again, we record an increase by entering the amount in the normal balance side of an account. The normal balance side of accounts payable, which is a liability, is the right (credit) side of the account so we increase accounts payable by entering the amount in the right side as a credit.

Entry 3

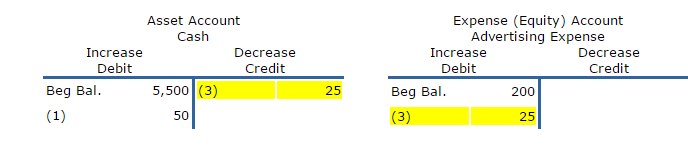

3. ABC places an ad in the local newspaper receives the invoice from the supplier and writes a check for $25 to the newspaper.

Source Document:Supplier’s Invoice and Company Check

Type Of Transaction:Cash Purchase

Accounts Affected:Advertising Expense (Equity) Cash

Debits and Credits:

Increase (Left Side) Advertising Expense (Decrease Equity): Debit

Decrease (Right Side) Cash: Credit

Explanation Using Our Debit/Credit Rules:

The Expense Account Advertising Expense is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of advertising expense, which is an expense account, is the left (debit) side so we increase advertising expense by entering the amount in the left side as a debit.

The Asset Account Cash is decreased.

We record a decrease by entering the amount in the opposite side of the normal balance side of an account. The normal balance side of cash, which is an asset, is the left (debit) side so we decrease cash by entering the amount in the opposite side which is the right (credit) side of the account as a credit.

Some additional clarification might be useful in order to clarify why an expense is recorded as an increase with a debit. The actual amount of the advertising expense has increased. The business now has spent more for advertising. More expenses are not what a business or an individual wants. Increased personal expenses reduce our personal equity and likewise increased business expenses reduce the owner’s equity of a business.

Since an increase in an expense reduces equity it is recorded as an increase using a debit.

Entry 4

4. ABC purchases five mowers for $10,000 and finances them with a note from the local bank.

Source Document:Bank Note

Type Of Transaction:Borrow Money

Accounts Affected:Mowing Equipment Note Payable-Bank

Debits and Credits:

Increase (Left Side) Mowing Equipment: Debit

Increase (Right Side) Note Payable-Bank: Credit

Explanation Using Our Debit/Credit Rules:

The Asset Account Mowing Equipment is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of mowing equipment, which is an asset account, is the left (debit) side so we increase mowing equipment by entering the amount in the left side as a debit.

The Liability Account Note Payable-Bank is also increased. Again, an increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of note payable-bank, which is a liability account, is the right (credit) side , so we increase note payable-bank by entering the amount in the right side as a credit.

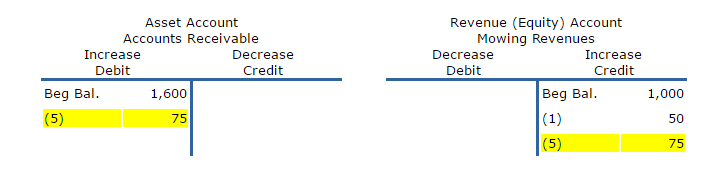

Entry 5

5. ABC mows another customer’s yard and sends the customer a $75 bill (invoice) for the

service they performed. They allow their customer ten (10) days to pay them for this service (on account).

Source Document:Sales Invoice

Type Of Transaction:On Account Sale

Accounts Affected:Accounts Receivable Mowing Revenue (Sales)

Debits and Credits:

Increase (Left Side) Accounts Receivable: Debit

Increase (Right Side) Mowing Revenue (Sales): Credit

Explanation Using Our Debit/Credit Rules:

The Asset Account Accounts Receivable is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of accounts receivable, which is an asset, is the left (debit) side of the account so we increase accounts receivable by entering the amount in the left side as a debit.

The Revenue Account Mowing Revenue (Equity) is also increased. Again, an increase is recorded

by entering the amount in the normal balance side of an account. The normal balance side of a revenue account is the right (credit) side of the account so we increase mowing revenue (sales) by entering the amount in the right side as a credit.

Entry 6

6. The owner of ABC needs a little money to pay some personal bills and writes himself a check for $500.

Source Document:Check

Type Of Transaction:Draw

Accounts Affected:Cash Draw

Debits and Credits:

Increase (left Side)Owner’s Draw (Decrease Equity): Debit

Decrease (Right Side) Cash: Credit

Explanation Using Our Debit/Credit Rules:

The Draw Account Owner’s Draw is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of owner’s draw, which is a draw account, is the left (debit) side so we increase owner’s draw by entering the amount in the left side as a debit.

The Asset Account Cash is also decreased. We record a decrease by entering the amount in the opposite side of the normal balance side of an account. The normal balance side of cash, which is an asset, is the left (debit) side so we decrease cash by entering the amount in the opposite side which is the right (credit) side of the account as a credit.

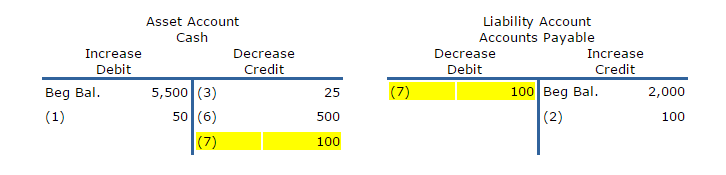

Entry 7

7. ABC pays the office supply company $100 with a check for the office supplies that they charged (promised to pay).

Source Document:Check

Type Of Transaction:Pay Supplier Charge Purchases

Accounts Affected:Cash Accounts Payable

Debits and Credits:

Decrease (Left Side) Accounts Payable: Debit

Decrease (Right Side) Cash: Credit

Explanation Using Our Debit/Credit Rules:

The Asset Account Cash is decreased. We record a decrease by entering the amount in the opposite side of the normal balance side of an account. The normal balance side of cash, which is an asset, is the left (debit) side so we decrease cash by entering the amount in the opposite side which is the right (credit) side of the account as a credit.

The Liability Account Accounts Payable is also decreased. We record a decrease by entering the amount in the opposite side of the normal balance side of an account. The normal balance side of accounts payable, which is a liability, is the right (credit) side so we decrease accounts payable by entering the amount in the opposite side which is the left (debit) side of the account as a debit.

Entry 8

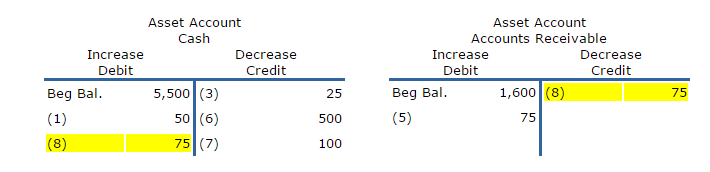

8. ABC receives a check from the customer who they billed (invoiced) $75 for services and allowed 10 days to pay.

Source Document:Customer Check

Type Of Transaction:Receive Customer Charge Payments

Accounts Affected:Cash Accounts Receivable

Debits and Credits:

Increase (Left Side) Cash: Debit

Decrease (Right Side) Accounts Receivable: Credit

Explanation Using Our Debit/Credit Rules:

The Asset Account Cash is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of cash, which is an asset, is the left (debit) side of the account so we increase cash by entering the amount in the left side as a debit.

Another Asset Account, Accounts Receivable decreased. We record a decrease by entering the amount in the opposite side of the normal balance side of an account. The normal balance side of accounts receivable, which is an asset, is the left (debit) side so we decrease accounts receivable by entering the amount in the opposite side which is the right (credit) side of the account as a credit.

We actually “swapped” one asset accounts receivable for another asset cash.

Entry 9

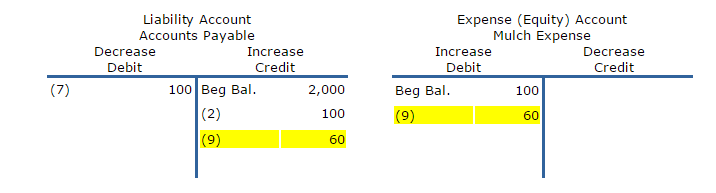

9. ABC purchased some mulch for $60 and received an invoice from their supplier who allows them 15 days to pay. The mulch was used on a customer’s yard.

Source Document:Supplier’s Invoice

Type Of Transaction: Purchase on Account

Accounts Affected:Mulch Expense Accounts Payable

Debits and Credits:

Increase (Left Side) Mulch Expense (Decrease Equity): Debit

Increase (Right Side) Accounts Payable: Credit

Explanation Using Our Debit/Credit Rules:

The Expense Account Mulch Expense is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of mulch expense, which is an expense account, is the left (debit) side so we increase mulch expense by entering the amount in the left side as a debit.

The amount owed to a supplier also increased.

The Liability Account Accounts Payable is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of accounts payable, which is a liability, is the right (credit) side of the account so we increase accounts payable by entering the amount in the right side as a credit.

Entry 10

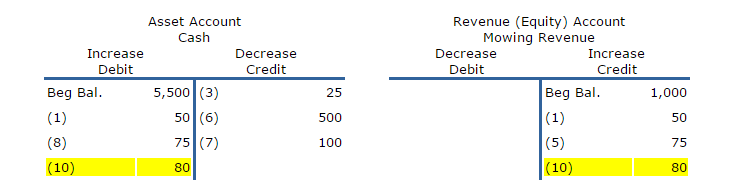

10. ABC bills (prepares an invoice) the customer $80 for the mulch and mowing his yard and

receives a check for $80 from the customer.

Source Document:Sales Invoice and Customer Check

Type Of Transaction:Cash Sale

Accounts Affected:Cash Mowing Revenue (Sales)

Debits and Credits:

Increase (Left Side) Cash: Debit

Increase (Right Side) Mowing Revenue (Equity): Credit

Explanation Using Our Debit/Credit Rules:

The Asset Account Cash is increased. An increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of cash, which is an asset, is the left (debit) side of the account so we increase cash by entering the amount in the left side as a debit.

The Revenue Account Mowing Revenue (Equity) is also increased. Again, an increase is recorded by entering the amount in the normal balance side of an account. The normal balance side of a revenue account is the right (credit) side of the account so we increase mowing revenue (sales) by entering the amount in the right side as a credit.

ABC’s Calculated Ending Account Balances After Posting

Me, being the nice guy that I am, calculated the ending account balances for you.

| Assets | Liabilities | Equity | |||

| Cash | 5,080 Dr | Accounts Payable | 2,060 Cr | Owner's Capital | 7,500 Cr |

| Accounts Receivable | 1,600 Dr | Note Payable-Bank | 10,000 Cr | Mowing Revenue | 1,205 Cr |

| Mowing Equipment | 12,500 Dr | Advertising Expense | 225 Dr | ||

| Inventory-Office Supplies | 100 Dr | Mulch Expense | 160 Dr | ||

| Owner Draws | 1,100 Dr | ||||

Let’s perform our checks on our ending balances after posting.

The first check is to see if our Accounting Equation balances and the second to make sure that the debit balances equal the credit balances.

Equation Check Calculations

Total Assets = Cash + Accounts Receivable + Mowing Equipment +Office Supplies

Total Assets = 5,080 + 1,600 + 12,500 + 100

Total Assets = 19,280

Total Liabilities = Accounts Payable + Notes Payable

Total Liabilities = 2,060 + 10,000

Total Liabilities = 12,060

Total Equity = Owner’s Capital + Revenues – Expenses – Draws

Since we have more than one expense let’s summarize them before we use them in our equation.

Total Expenses = Mulch Expense + Advertising

Total Expenses = 160 + 225

Total Expenses = 385

Total Equity = Owner’s Capital + Revenues – Expenses – Draws

Total Equity = 7,500 + 1205 – 385- 1100

Total Equity = 7,220

Substituting our totals into the Accounting Equation we find that our equation balances.

Assets = Liabilities + Owner’s Equity

19,280 = 12,060 + 7,220

Our second check is to see if our debit account balances equal our credit account balances.

Let's Total Our Debit Balances

| Debit Balance Accounts | ||

| Cash | 5,080 | |

| Accounts Receivable | 1,600 | |

| Mowing Equipment | 12,500 | |

| Inventory-Office Supplies | 100 | |

| Advertising Expense | 225 | |

| Mulch Expense | 160 | |

| Owner's Draw | 1,100 | |

| Total Debits | 20,765 | |

Now, we'll Total Our Credit Balances

| Credit Balance Accounts | ||

| Accounts Payable | 2,060 | |

| Note Payable-Bank | 10,000 | |

| Owner's Capital | 7,500 | |

| Mowing Revenue | 1,205 | |

| Total Credits | 20,765 | |

Looks like everything is still in balance after we posted our transactions.

Assets = Liabilities + Owner’s Equity and our Debit Balance Accounts = our Credit Balance Accounts.

That wasn't too bad was it ? Get a grip on yourself. We still have more lessons to complete. After the Videos and Tests let's tackle the next lesson that covers the General Ledger and Journals.