Analyze Transactions Transcript

Accounting Cycle > Analyze Transactions

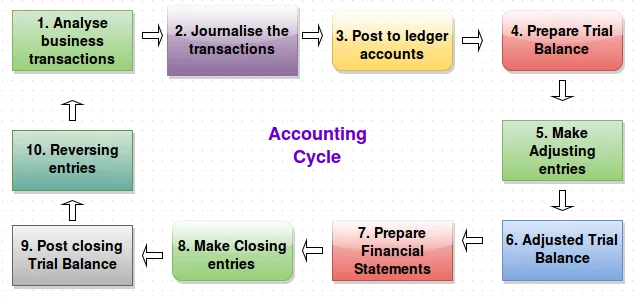

The Accounting Cycle is the foundation of Financial Accounting and almost all accounting.

Regardless of what type of accounting you're interested in, it all starts with the accounting cycle.

The steps are: analyze transactions; journalize transactions; post transactions to the ledger; prepare an unadjusted trial balance; journalize and post adjusting entries;

prepare the adjusted trial balance; prepare financial statements; journalize and post closing entries; and then the 9th and 10th optional steps, prepare a post closing trial balance and reversing entries (not covered).

Professor Alldredge has devoted many of his video lectures to these steps in order to help you master the accounting cycle.

Let's start with the first step.

Analyzing transactions is a three part process.

Part one is identifying the accounts affected and what type of accounts they are.

Part two is determining which accounts are increasing and/or decreasing.

And part three is applying the rules of debits and credits to these accounts.

Let's do a couple of examples to show you how you'll want to analyze transactions in your assignments.

Example, company buys supplies on account.

So part one is identify the accounts affected and what accounts they are.

In this example the accounts are supplies, an asset account, and accounts payable, a liability account.

Part two is determine, which accounts are increasing or decreasing.

In this example, supplies is increasing because we have more supplies after this transaction than we had before.

Accounts payable is also increasing because we owe more money after this transaction than we did before.

Part three is applying the rules of debits and credits to these accounts.

Here's where you'll need to know the debit and credit rules.

Supplies is an asset accountant and assets are increased with debits.

Accounts payable is a liability account and liabilities are increased with credits.

Let's look at another example.

Company performs service on account.

Part one is identify the accounts affected and the type of accounts they are.

In this case the accounts are accounts receivable, an asset account, and service revenue, a revenue account.

Part two is determine which accounts are increasing or decreasing.

Accounts receivable is increasing because we have more money owed to us after this transaction than we had before.

Service revenue is also increasing because we've earned more revenue after this transaction and we did before.

Part three is apply the rules of debits and credits to these accounts.

Accounts receivables is an asset and assets are increased with a debit.

Service revenue is a revenue and revenues are increased with credits.

Let's look at one more example - something a little bit different.

A company pays a utility bill.

Part one is identify the accounts affected and what type of account they are.

The accounts are cash, an asset account, and utilities expense, an expense account.

Part two is determine which accounts are increasing or decreasing.

Cash is decreasing because we have less cash after paying this bill than we had before.

Utilities expense is increasing because we've incurred more expense after this transaction than we did before.

Part three is apply the rules of debits and credits to these accounts.

Cash is an asset and assets are decreased with a credit.

Utility expense is an expense and expenses are increased with debits.